PI insurance policies and cover

- Are longer term PI policies available this year?

- Should I consider an 18-month policy?

- What kinds of claims does PI insurance cover – are there any exclusions?

- Does professional indemnity insurance cover everyone in the firm?

- What limit of professional indemnity do I need?

- What factors should I consider when assessing the level of cover we need for our PI exposure?

- How does the aggregation clause work

- What are the most common causes of PI claims against law firms?

- Which practice areas generate the most professional indemnity claims?

- What is ‘claims made’ cover and what implications does it have?

- What is the difference between a PII ‘claims made’ policy and a ‘claims occurring’ wording used in other insurances?

- Can I extend the Extended Policy Period (EPP) and continue taking new instructions?

- Should my firm increase its excess to try and reduce the overall PII premium?

- Are my legal defence costs covered when a claim occurs?

- Will my excess apply to legal defence costs?

- Does my policy pay for legal costs if an investigation is brought by the SRA?

- Should I buy cyber insurance as well as PII?

- Should I buy management liability cover in addition to PI insurance?

- How do I check the rating of my insurer and why is this important?

- I am 65 with no succession plan in place. Why won’t an alternative insurer provide a quote for me?

- How does the Solicitors Indemnity Fund (SIF) operate?

Closing down a legal practice

- I may pack up my law firm and become a freelancer, what do I need to do?

- Run-off cover – how does it work and what do I need to know?

- Why is run-off so expensive?

- How much will I pay for six-year run-off cover if the firm should need to close?

- Can I get an alternative run-off quote?

- Can I pay my run-off premium by instalments?

Other special situations

- What information do insurers want if I am a new start up?

- I am converting into an LLP. Can I transfer my PI insurance to the new firm?

- I am considering acquiring a practice known to me. What information do I need to provide the insurer with?

Handling PI insurance claims

- What claims support does the broker provide?

- How can a broker’s involvement on a claim be beneficial to the outcome for my firm?

- Why are we asked not to disclose insurers' involvement when a claim arises?

- Why am I not allowed to admit liability without the insurer’s consent?

- Why am I not allowed to make an offer of settlement without the insurer’s consent?

Jargon buster, professional indemnity insurance

- What is Minimum Terms and Conditions (MTC) cover?

- What is the Extended Policy Period (EPP)?

- What is retroactive cover?

- What is an aggregate capped excess?

- What does ‘insurers are re-allocating capacity’ mean?

- What is an insurance broker’s ‘exclusive insurance facility’?

- What is ‘wholesale’ broking and what does it mean for my firm?

- What is a ‘co-insurance’ facility and what are the benefits to my firm?

- What is ‘broker duplication’?

- What is a Managing General Agent (MGA)?

- What is the Participating Insurers Agreement (PIA)?

- What are reserves and how do they affect my premiums?

The four experts

Law Firm Ambition is grateful to the four specialist legal sector insurance brokers who collaborated with us to come up with this long list of FAQs and answers. (Updated 1 September 2025)

Brian Boehmer is a partner at Lockton.

Neil Pointon is a divisional director at Howden.

Gary Horswell is the managing director of Ntegrity.

Dan Blundell is a senior vice president at Paragon.

PI insurance policies and cover

1. Are longer term PI policies available this year?

Longer term policies are now widely available again, pleasingly not only for lower risk firms.

But for firms that are in periods of change, these may not be available. For example, firms experiencing significant growth, or significant claims activity, or a change in leadership or the profile of work.

Brian Boehmer, partner, Lockton

2. Should I consider an 18-month policy?

As we see the start of a softening market, extended policies are being offered to many more firms. This is not every firm though, and some insurers will not offer 18-month options for new business, but we are certainly seeing a move back to the pre-Covid norm in this area.

If the market continues to soften, you should consider whether an annual policy may save your firm money.

Many firms value the certainty of knowing where they stand for the longer policy period. But, in contrast to recent years, if insurers are offering longer policies at a flat pro-rata premium it is likely that they think the premiums will continue to come down.

Dan Blundell, senior vice president, Paragon

3. What kinds of claims does PI insurance cover – are there any exclusions?

Primary PII cover is designed to provide broad coverage to protect the general public along with the reputation of the legal profession. The ‘Minimum Terms and Conditions’ (MTC) wording set by the SRA guarantees this.

In the event of a claim being made by a third party, arising from your practice’s provision of legal services, your firm can be confident that they are properly insured. The claim could arise from an alleged negligent act or omission, defamation, or a breach of trust and/or confidentiality.

But whereas the exclusionary language is minimal in the MTC wording, the same is not necessarily true of any additional insurance that is purchased. Insurers are permitted to apply exclusions.

So, a firm may end up with cover up to a certain limit for a particular claim, but no cover beyond that limit if the claim is excluded from the additional layer(s) of insurance.

1st party cyber risk is typically excluded from all PII coverage now, including for the legal profession. This is not a restriction of coverage, as there was no intended provision of the coverage.

Regulatory matters are typically excluded too, so discuss this particular exposure with your insurance broker.

Brian Boehmer, partner, Lockton

4. Does professional indemnity insurance cover everyone in the firm?

Yes, the policy provides cover for claims against current and past principals, staff and consultants.

Gary Horswell, managing director, Ntegrity

5. What limit of professional indemnity do I need?

See: In light of the cost, should I consider lowering my limit of indemnity? in Professional indemnity insurance for law firms FAQs: Part one

6. What factors should I consider when assessing the level of cover we need for our PI exposure?

Key factors include:

- Your practice’s likely level of exposure to claims – influenced by the practice areas undertaken and your typical clients.

- The nature of activities undertaken which could expose your practice to risk, including the nature and level of undertakings accepted.

- Your practice’s claims history, especially if there are any particular trends that can be identified.

- The maximum value possible for a single claim, influenced by your largest transaction values undertaken, or the entirety of the value of an estate.

- The total value if a series of claims from related events were to occur (aggregation, see 7).

- The total amount of money in your client account at any given time. Your PII limit should reflect at the very least the average amount in the account at any given time.

Claims are covered by the insurance in place at the time of notification, but can take years to settle. Will today’s limit be adequate to settle a claim being paid finally in, say, 5 years’ time?

Whatever the limit of indemnity in the policy, this is the maximum insurers will pay to a claimant, so it needs to allow for the compensation payable and the claimant’s legal costs (defence costs are typically not covered).

Brian Boehmer, partner, Lockton

7. How does the aggregation clause work

The aggregation clause in the SRA’s Minimum Terms and Conditions potentially allows multiple claims to be treated as a single claim, for the purpose of applying the limit of indemnity under the policy, provided the claims arise from:

- one act or omission

- one series of related acts or omissions

- the same act or omission, in a series of related matters or transactions

- similar acts or omissions, in a series of related matters or transactions

- one matter or transaction

For example, your firm acts for 10 purchaser clients in a new build development. The identical contracts for sale, prepared by the developer’s solicitors, contains a clear error which you fail to spot. This results in each of your clients suffering a loss of £1m, which they claim against you (so £10m in total). Your firm has a £3m limit of indemnity under your PII policy. If the claims can be shown to aggregate into one claim, your insurer will only have to cover the first £3m, leaving your firm to pay the balance (or your excess layer insurers to pay it, if you have this additional cover).

Insurance claims involving aggregation disputes with insurers are extremely fact-specific and the outcomes are often far from clear (so more often than not leading to settlements) but, given your firm’s potential exposure, this is a factor to consider when deciding the appropriate level of cover for your firm.

Neil Pointon, divisional director, Howden

8. What are the most common causes of PI claims against law firms?

The most common current causes of claims include:

- Failure to properly record instructions (no/poor engagement letter, scope of retainer).

- Lack of file notes.

- Missed time limits.

- Lack of supervision, or failure to seek assistance.

- Advising outside your area of expertise.

- Conflicts of interest.

- Time pressures.

- Mental health and wellbeing of fee-earners.

- Cyber security issues. (See 17 )

Of course, an underlying factor is client selection. Clients who are particularly demanding or awkward to deal with, or who put your fee-earners under unreasonable pressure, are more likely to make a claim.

See: What types of legal work increase premiums the most (and least)? in Professional indemnity insurance for law firms FAQs: Part one

See also: Five highly practical factsheets explaining how to avoid professional negligence claims in residential conveyancing, wills and probate, commercial property, company and commercial, and commercial litigation.

Neil Pointon, divisional director, Howden

"Over recent years we have seen an increase in the volume of the errors leading to PI claims. The underlying causes are primarily fee-earners being stressed, fatigued, over-worked, or under pressure, whether at home or at work."

Philippa Wilkin, senior risk management consultant, Travelers

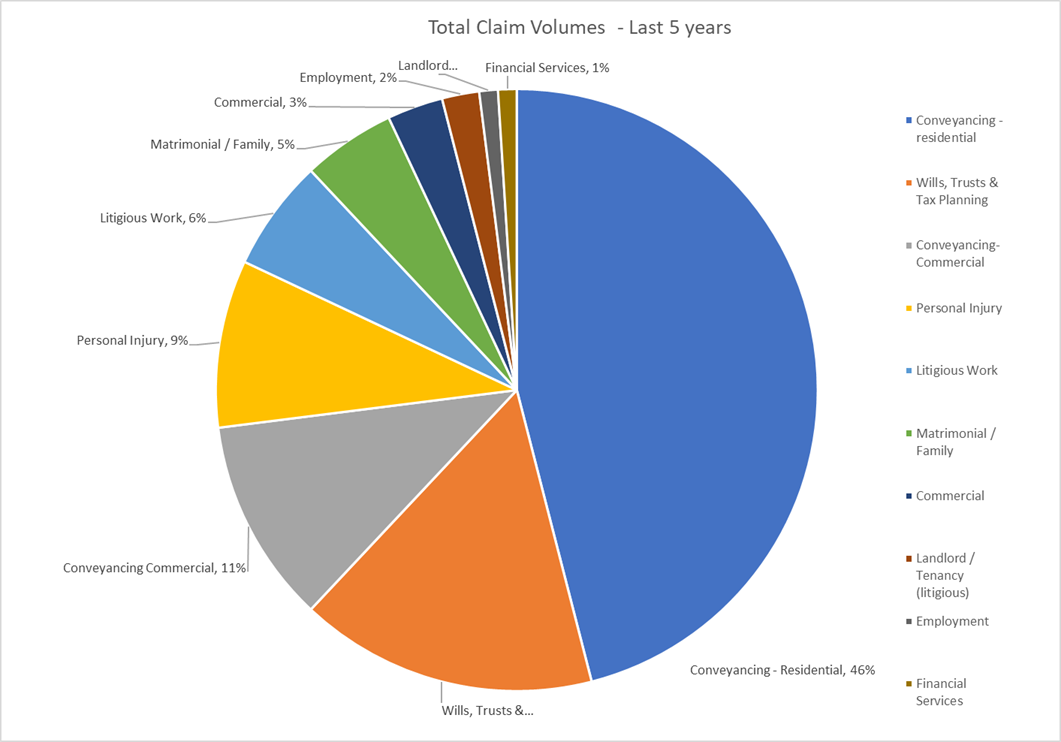

9. Which practice areas generate the most professional indemnity claims?

The diagram below is a good illustration. It shows that in the last five years of claims data (2019-2024) the number of claims notified (not claims payments)could be broken down into the following practice areas:

- 46% Residential conveyancing

- 16% Wills, probate, trusts

- 11% Commercial conveyancing

- 9% Personal injury litigation

- 6% Litigious work

- 5% Matrimonial/family

- 3% Commercial

- 2% Employment

- 1% Landlord and tenant

- 1% Financial advice and services

Source: Lockton Companies LLP

Brian Boehmer, partner, Lockton

"While conveyancing tops the list above, errors can creep into all practice areas. 'Risk aware' firms actively identify and manage the risks that lead to errors, which can reduce or avoid PI claims."

Philippa Wilkin, senior risk management consultant, Travelers

10. What is ‘claims made’ cover and what implications does it have?

PI insurance policies protect the insured firm against claims that are first made against them during the policy period. This remains true even if the work giving rise to the claim was done by the law firm years before.

PI insurance is often referred to as “long tail liability”, as it can take several years before a loss to a client crystallises and turns into a notification of a claim.

Each year, your law firm is effectively insuring all of its past work that could yet result in a claim. (This is why insurers ask for details of the fees and claims from previous years.)

Brian Boehmer, partner, Lockton

11. What is the difference between a PII ‘claims made’ policy and a ‘claims occurring’ wording used in other insurances?

As explained in 10 above, a ‘claims made’ policy covers claims notified to insurers during the policy period, even if the work giving rise to the claim was done by the law firm years before.

In contrast, a ‘claims occurring’ policy covers injury or damage sustained during the policy period, even if the claim does not arise until years later.

Two examples make this easier to understand.

A law firm that receives a claim today about a will that it wrote 50 years ago will be covered by the PI insurance cover in place today, because PI cover is on a ‘claims made’ basis.

Whereas a building firm that receives a claim today about employer’s liability regarding asbestos work done 50 years ago will be covered by any employer’s liability insurance that was in place 50 years ago (assuming that the current building firm is the same legal entity as the one 50 years ago, and assuming that the insurance is traceable).

Gary Horswell, managing director, Ntegrity

12. Can I extend the Extended Policy Period (EPP) and continue taking new instructions?

In response to the pandemic, the indemnity rules were changed to allow firms facing practical difficulties in obtaining indemnity insurance to apply for a waiver to extend the EPP/Cessation Period – provided their insurer agreed to that extension. However, insurers are generally reluctant to grant the extension.

But the key point about EPP is to avoid it in the first place. Given the increased due diligence undertaken by insurers and the potential slower response times, there is all the more reason to return your proposal form to your broker (or insurer) as early as possible to secure your insurance cover.

Understandably, insurers view EPP negatively, especially if there is no legitimate reason for entering it. Some insurers will not quote a practice that has fallen into it.

However, for firms that are having difficulty getting insurance cover, perhaps because of especially challenging circumstances, the SRA’s change to the rules offers a potential lifeline. It may help firms to continue to take new instructions while they seek cover, particularly if they can extend the initial 30-day period.

Brian Boehmer, partner, Lockton

13. Should my firm increase its excess to try and reduce the overall PII premium?

Increasing your excess could perhaps reduce your premium, but firms often find that it does not achieve the level of reduction they had expected.

Another crucial factor is affordability. A firm’s policy will typically have a ‘capped’ excess: for example, £10,000 x 3 means that you will have to pay a maximum of £30,000 in excess payments during the policy period, regardless of the number and value of claims made against you.

You should budget for this maximum amount because, if you fail to pay any excesses due within 30 days, the insurer is obliged to pay them on your behalf. Your insurer is also obliged to report this to the SRA, which could lead to regulatory issues – and your insurer having concerns about the financial stability of your firm could adversely impact your next PII renewal. You would also have to declare this issue when applying for PII in future years.

In the current soft market conditions, it usually makes commercial sense to reduce your excess payments, rather than increase them.

Neil Pointon, divisional director, Howden

14. Are my legal defence costs covered when a claim occurs?

Yes. Legal defence costs pre-authorised by the insurer are covered. So always approach your insurers for authorisation in advance of engaging professionals and obtain written approval for incurring any costs.

The exception is if an investigation is brought by the SRA (see 16).

The issue of ‘reasonable and necessary costs’ is covered in the SRA’s Minimum Terms and Conditions (see 2).

Dan Blundell, senior vice president, Paragon

15. Will my excess apply to legal defence costs?

No, your defence costs (legal and other costs) are covered by your policy and must be paid by the insurer under the SRA’s Minimum Terms and Conditions rules.

Neil Pointon, divisional director, Howden

16. Does my policy pay for legal costs if an investigation is brought by the SRA?

No, typically your PII policy will not provide cover for these costs unless explicitly stated as an extension of the standard wording.

Some PII policies pay for legal costs of an SRA investigation provided there is a potential claim from a third party under your PII policy.

But if the enquiry is a pure conduct matter with no potential third-party claim, this is a risk that can be covered by a separate Management Liability Protection policy that sits alongside your PI insurance policy.

Gary Horswell, managing director, Ntegrity

17. Should I buy cyber insurance as well as PII?

All law firm clients should consider taking out a cyber policy in addition to their PII. While a solicitors’ PII policy provides cover for legal liability arising out of private practice as a result of a cyber event, only third-party loss is covered, so it will not cover any costs and expenses of dealing with a cyber event. These include reporting to the ICO and communicating with affected clients, engaging specialists to provide support, assistance and remediate systems, and other losses relating to the interruption to your business, which can be significant.

Some insurers currently require you to have separate cyber insurance before they will offer you terms for PII, although this is technically not permitted under the Participating Insurers Agreement (PIA).

The cost of cyber insurance is modest compared with PII, and cyber policies tailored for law firms are widely available in the market. Your broker will be able to advise you on the most suitable policy for your firm’s profile. The recent reduction in PII rates has led some firms to use the premium saving to purchase cyber insurance for the first time, with no overall increase in insurance outlay.

Neil Pointon, divisional director, Howden

"Law firms have a duty of care, and a reputation, for safe handling of personal data and financial transactions. Cyber crime can affect both, in ways that may not be covered by a PI policy, so standalone cover should be considered a 'must have'."

Philippa Wilkin, senior risk management consultant, Travelers

18. Should I buy management liability cover in addition to PI insurance?

Professional indemnity insurance covers claims brought against the firm. Whereas management liability cover (called a Directors and Officers policy, or D&O) covers any claims brought against individuals in a firm in a management position.

Typically, the policy protects the partners/directors/members, the COLP and the COFA as individuals. It can also include entity cover, in case proceedings are brought against the firm. In a heavily regulated sector such as legal services, the risks of such a lawsuit are higher than in a less regulated business.

Like a cyber policy, it is not a mandatory insurance, but it is a product a firm should certainly consider.

Dan Blundell, senior vice president, Paragon

19. How do I check the rating of my insurer and why is this important?

You can check the financial rating of your insurer by checking the list of participating insurers on the SRA’s website. It is important to have an insurer that has a strong financial rating, so you can be confident that it will be around and able to pay any claims you may have.

Having a strong financial rating should also increase an insurer’s longevity in providing PII to the legal profession and so reduce the chances of a law firm becoming 'orphaned' by an insurer’s decision to pull out of the solicitors’ PII market at a future renewal (as has happened in the past).

The SRA has declined to require participating insurers to have a minimum financial rating (unlike other regulators, such as the Royal Institution of Chartered Surveyors). So it is doubly important to make sure you are comfortable with the financial strength of your PII provider.

Currently, there are no unrated participating insurers. As a result, financial rating is a lesser concern than it has been in the past.

Neil Pointon, divisional director, Howden

20. I am 65 with no succession plan in place. Why won’t an alternative insurer provide a quote for me?

In this scenario, it is likely that sooner or later the firm will cease to trade if it is not acquired by another firm. And a firm that may soon cease to trade is not an attractive proposition for any new insurer. For a start, the insurer is likely to end up ‘on the hook’ for six years of run-off cover. (See 23)

Insurers are ideally looking for professionally run firms that have a viable business model and plans for the short, medium and long term. Renewing the insurance each year for such firms is relatively straightforward and the risk of claims arising tends to be lower.

Succession is an obvious issue for any sole practitioner. If the firm’s owner is reaching retirement age with no succession plan in place, getting PI insurance may be more difficult.

Brian Boehmer, partner, Lockton

21. How does the Solicitors Indemnity Fund (SIF) operate?

The Solicitors Indemnity Fund (SIF) acts as an important safety net, providing ‘expired run-off cover’.

This cover is to deal with any claims that arise once the six-year run-off cover has expired, as claims can happen 15 or even 25 years or more after closure.

Solicitors Indemnity Fund explained

The Law Society (of England and Wales) established the Solicitors Indemnity Fund in 1987 to provide compulsory professional indemnity cover to solicitor firms in private practice.

In 1999 the solicitor’s profession elected to move towards an insurance-based open market scheme, with the consequence that SIF entered into run-off with effect from 1 September 2000.

With the agreement of The Law Society, SIF has provided ‘expired run-off cover’ to firms that ceased without a successor since 1 September 2000, but only after the primary run-off period of six years had elapsed.

The Solicitors Regulation Authority took over the management of SIF on 1 October 2023. It was previously managed by the Law Society, through a specialist team set up for this purpose.

SIF is funded by mandatory annual contributions from solicitors and law firms. These are typically calculated based on the size and type of practice, the number of partners, and sometimes the claims history of the firm.

Gary Horswell, managing director, Ntegrity

Closing down a legal practice

22. I may pack up my law firm and become a freelancer, what do I need to do?

You would be required to purchase run-off cover for the closure of the regulated practice (see 23).

Whether or not you need to buy PII as a freelance solicitor depends on the work you will be undertaking.

If you are only going to be undertaking non-reserved legal activities, the SRA permits freelance solicitors to provide services direct to clients without any PII in place (although you have to inform clients of this and be certain that they understand this and are still happy to instruct you anyway). Although not compulsory, it is advisable to obtain appropriate PII cover to protect you and your personal assets in the event that a successful claim is made against you.

If you will be undertaking reserved legal activities, you must obtain ‘adequate and appropriate’ PII cover. Although this does not have to be MTC-compliant, if it is not your clients must be made aware of this before engagement. As there are still relatively few freelance solicitors (just 650 according to the SRA in 2024), only a few insurers currently provide cover for freelance solicitors.

Neil Pointon, divisional director, Howden

"If you fit the SRA's definition of a 'freelancer', speak to your insurance broker about freelance policies. As ever, consider the reputation of the insurer and price, but also the breadth of cover of the policy."

Philippa Wilkin, senior risk management consultant, Travelers

23. Run-off cover – how does it work and what do I need to know?

Once a firm stops practising (and there is no successor practice responsible for insurance) the insurer covering the firm at the time of closure must provide six years of run-off cover. This will provide the firm with six years of additional cover from the end of a current policy following the date of closure. (After the six years, the Solicitors Indemnity Fund (SIF) takes over the cover (see 21).)

On being advised that the firm will cease to trade from a particular date, the insurers will bill the practice for the run-off premium due.

Any retrospective claims that are brought against the firm are covered by the insurer. The owners of the firm have no ongoing liability.

Typically, run-off cover will cost between 200-350% of your expiring premium (check your wording). For example, a firm that paid £20,000 + tax at their last renewal would pay £60,000 + tax for their run-off cover (assuming the run-off, as set in the policy, was 300%). The cost of run-off must be disclosed to the firm during the insurance quotation process.

Run-off cover is a contractual duty for insurers. Put simply, in the example above the insurer is obliged to take on six years of claims exposure in return for three years of premium – which is not an attractive proposition. So the likelihood of being asked to provide run-off cover is one of many risk factors that insurers weigh up when pricing PI insurance cover for a law firm.

See also: The Travelers run-off calculator and its related notes.

Brian Boehmer, partner, Lockton

24. Why is run-off so expensive?

Run-off cover is expensive because it must account for the long-tail nature of PII claims in legal practice. Once a law firm ceases trading, the risk of claims doesn't disappear. Clients may bring negligence claims years after the work was done (up to 15 years under the Limitation Act 1980), often in areas such as conveyancing or probate, where errors may only surface much later.

Insurers pricing run-off cover must anticipate potential liabilities and reserve capital for potential claims over a six-year period after a firm has closed (as required by the SRA Minimum Terms and Conditions), with no opportunity for the insurer to reassess risk or adjust premiums annually.

Run-off cover is priced as a one-off premium, typically between 225 – 350% of the last annual premium. This reflects the insurer’s need to cover all liabilities without further premium income from the firm. Insurers also face challenges in defending claims against closed firms due to limited access to personnel and documentation. It also takes into account the fact that many firms fail to pay for run-off cover, but the incumbent insurer is obliged to provide it regardless of payment.

Neil Pointon, divisional director, Howden

25. How much will I pay for six-year run-off cover if the firm should need to close?

The premium for six-year run-off cover varies between insurers. It is generally 300% of the last annual premium, but it can range from 150-400%.

It is payable in full prior to the date of closure.

When quoting for your PII renewal, all insurers should advise you of the calculation for the run-off cover premium in the event that your firm closes.

Brian Boehmer, partner, Lockton

26. Can I get an alternative run-off quote?

While not unheard-of, insurers generally will not compete to take over run-off cover. It is felt that the best insurer for the run-off risk is the one insuring the risk when the law firm last renewed.

Dan Blundell, senior vice president, Paragon

27. Can I pay my run-off premium by instalments?

The official answer to this is no. Most insurers require a single payment in full upfront, because once a firm ceases it is no longer bringing in revenue.

However, if you are unable to pay the premium in full, speak to your insurer. As your insurer is obliged to provide run-off cover regardless of whether or not it has been paid for, it may be willing to accept instalment payments where it has sufficient comfort that future payments will actually be made.

Neil Pointon, divisional director, Howden

Other special situations

28. What information do insurers want if I am a new startup?

For a start-up practice an insurer will need the following information as a minimum:

- Proposal form

- Business plan

- Profit & Loss forecast

- Cash flow forecast

- CVs of all partners/directors/members of the new practice

Gary Horswell, managing director, Ntegrity

29. I am converting into an LLP. Can I transfer my PI insurance to the new firm?

There is no need to transfer the policy. You remain liable for claims arising against the previous entity. The solution is simply to add the new LLP to the ‘insured’ named in the policy.

The minimum limit of indemnity you are obligated to buy (as set by the SRA) will increase from £2m to £3m. If your current limit is below £3m, normally your insurer will charge an additional premium for the increased cover on a pro rata basis for the length of time remaining on the policy.

Dan Blundell, senior vice president, Paragon

30. I am considering acquiring a practice known to me. What information do I need to provide the insurer with?

Early engagement with your broker and insurer is essential.

The first consideration is whether your firm will be deemed to be the ‘successor practice’ to the other firm. If so, your firm will assume liability for all future claims made against that firm, including those arising from historic work undertaken by the acquired firm. If not, the selling firm must arrange run-off cover (see 23).

Secondly, insurers will expect detailed information to assess the risk and structure of the acquisition, including:

- Your due diligence findings

- The financial and cashflow impact

- The acquired firm's claims history

- Its last completed proposal form and any supporting documentation

- The complexity of the transaction

- A robust integration plan

Insurers will also want clarity on the nature and purpose of the acquisition. Are you simply acquiring a client book in a niche area in which you already specialise, or are you expanding into a new area (or areas) of practice? Differences in office locations, staffing, IT infrastructure, legal services, client types and firm cultures can all introduce risk. Your plan should acknowledge these challenges and outline a credible strategy for managing them

Neil Pointon, divisional director, Howden

"Provide your broker with as much detail about the potential acquisition as you can. Your insurer can then understand, discuss, and confirm how the acquisition might impact your PI insurance."

Philippa Wilkin, senior risk management consultant, Travelers

Handling PI insurance claims

31. What claims support does the broker provide?

A specialist broker will usually have a dedicated specialist claims team. The claims advocates will support clients in all aspects of claims handling:

Some insurers also have specialist panel solicitors who are appointed automatically in the event of a claim been made.

A specialist broker with strong relationships with all of the leading insurers should be familiar with their individual approaches to policy interpretation. This in turn will affect how best to approach a particular issue.

Brian Boehmer, partner, Lockton

32. How can a broker’s involvement on a claim be beneficial to the outcome for my firm?

A specialist broker claims team can provide proactive advice at every stage, starting before notification of the claim.

Knowing the insurer’s likely tactics and strategy, the broker can provide valuable advice and assistance dealing with a claim.

This may include advice on any ‘reserves’ requested by the insurers. (See 47)

Brian Boehmer, partner, Lockton

33. Why are we asked not to disclose insurers' involvement when a claim arises?

Insurers prefer their involvement not to be disclosed earlier than necessary.

This is because, historically, insurers have had a reputation for settling most claims quickly rather than incurring the significant cost of fighting a claim. So early disclosure can encourage the claimant to pursue the claim more vigorously.

Instead, insurers prefer to have some time to analyse a claim in the first place and understand if the insured law firm is actually liable.

Dan Blundell, senior vice president, Paragon

34. Why am I not allowed to admit liability without the insurer’s consent?

Most solicitors’ PII policies contain what is known as a ‘claims control’ clause – essentially meaning that insurers have the right to take over the conduct of any claim or circumstance notified to them and handle it as they see fit.

This will include a requirement not to admit liability without the insurer’s consent, for a number of reasons:

- It gives insurers an opportunity to investigate the matter and to determine whether or not liability ought to be admitted.

- What frequently happens is that a firm admits liability and makes an offer of settlement to an important client in order to maintain a commercial relationship, even where the firm may not actually be liable for any loss the client may have suffered.

- Some insurers have obligations under their reinsurance arrangements that prevent them from allowing a firm to admit liability until the primary layer insurer’s claims department has determined that the firm is indeed liable.

Your insurer is only obliged to indemnify you when you are actually liable in respect of a PII claim. If you admit liability and make a payment to a client and it subsequently transpires that you are not in fact liable, your insurer has no duty to reimburse you.

Neil Pointon, divisional director, Howden

35. Why am I not allowed to make an offer of settlement without the insurer’s consent?

It is a term of most solicitor professional indemnity policies that insurers have the right to take over defence of a claim. That includes making an offer of settlement.

Insurers insist on being involved in claim settlements because they have the specialist expertise and they will be the organisation making the payment.

The insurer will want to confirm that there is no further exposure to liability, that any settlement sum is reasonable, and that any settlement will close the dispute properly.

An offer of settlement without the insurer’s prior express consent runs the risk of the insurer asserting that its rights have been prejudiced – so its obligation to pay the claim is altered.

Gary Horswell, managing director, Ntegrity

Jargon buster, professional indemnity insurance

36. What is Minimum Terms and Conditions (MTC) cover?

MTC cover refers to the mandatory minimum requirements that all PII policies must meet for SRA-authorised law firms in England and Wales. These terms are set out in an appendix to the SRA Indemnity Insurance Rules and are designed to ensure consistent, robust protection for law firms, clients and the public, regardless of which participating insurer provides the cover.

Importantly, however, the MTCs do not prescribe the level of cover a firm ought to have, nor the level of its excess. Firms have a regulatory requirement to ensure they have ‘adequate and appropriate’ insurance under the SRA Indemnity Insurance Rules and the level of excess is at a firm’s discretion, subject to insurer agreement.

Neil Pointon, divisional director, Howden

37. What is the Extended Policy Period (EPP)?

The Extended Policy Period is for law firms that are unable to obtain insurance in the open market by the renewal date of their existing policy. This can result from a deterioration of the firm’s risk profile, or a change of strategy/focus on the part of the insurer.

EPP runs for 90 days and operates as follows:

Firms facing practical difficulties in obtaining indemnity insurance can apply for a waiver to extend the EPP/Cessation Period – but only if their insurer has agreed to that extension. (See 12)

Background

The Extended Policy Period (EPP) was previously known as the Extended Indemnity Period (EIP), which in turn was created as the solution to the problematic Assigned Risk Pool (ARP) back in 2013.

The problem was that firms with a poor claims record entered the ARP but then never managed to exit. Instead, they carried on trading and the claims count kept increasing. This caused huge losses for the insurers who were left ‘on the hook’ to pay for it all. This in turn led to insurers leaving the market and increased premiums for firms with a good claims record.

Gary Horswell, managing director, Ntegrity

38. What is retroactive cover?

Retroactive cover is the cover given for work undertaken in the past.

It means that work you completed before you took out your policy can be covered by your PI insurance, as long as it was undertaken after the retroactive date. Typically, this would arise when a firm starts up, with any PI insurance commencing from the date of establishment.

Brian Boehmer, partner, Lockton

39. What is an aggregate capped excess?

An aggregate capped excess is the total maximum liability that your law firm is exposed to contribute towards claim settlements during the policy period. It is designed to limit the amount you pay in a year of several claims.

Take the example of a firm with a £10,000 excess capped at £30,000 in the annual aggregate, for a 12-month insurance policy. In a year with five claims of over £10,000 each, the firm will pay a £10,000 excess for each of the first three claims, but nothing after that.

Policies that are longer than 12 months typically use a pro rata calculation. So in the example above, an 18-month policy would have the same £10,000 excess, but would be capped at £45,000 in the aggregate for the 18 months.

Brian Boehmer, partner, Lockton

40. What does ‘insurers are re-allocating capacity’ mean?

Insurers operate with a finite pool of capital, which they allocate across different markets based on expected returns and risk appetite. Each year, they reassess where to deploy this capital, increasing investment in sectors that appear profitable and reducing exposure in areas where returns are declining.

This strategic shift is known as 're-allocating capacity'. In practical terms, once an insurer reaches its target level of premium income for a specific market – such as solicitors’ PII – it may stop accepting further new business in that area.

By managing their exposure in this way, insurers aim to maintain financial stability and ensure they can meet claims obligations across their portfolios. For law firms, this means that the availability of cover can fluctuate depending on broader market conditions and insurer strategy.

Neil Pointon, divisional director, Howden

41. What is an insurance broker’s ‘exclusive insurance facility’?

An exclusive facility is an insurance arrangement that can only be accessed through a specific broker. This means that if you firm wants to benefit from that facility’s term or pricing, you must access it through that particular broker.

Insurers may offer such exclusivity to manage the volume and quality of submissions, often preferring to work with brokers who understand the market and can filter out less attractive risks. An exclusive broker’s role is to act as a gatekeeper, presenting insurers with risks that are most likely to meet underwriting criteria.

No single broker has access to every insurer offering PII to law firms. Some brokers claim to have access to the entire market, but then simply forward your proposal to those brokers who actually do hold the insurer relationships.

Understanding who truly has market access – and whether they offer exclusive facilities – can help your firm secure better terms and pricing.

Neil Pointon, divisional director, Howden

42. What is ‘wholesale’ broking and what does it mean for my firm?

If you use a local general broker to arrange PII and other insurances, they may well send your PII proposal to a wholesale broker.

Wholesale brokers are usually volume operators who will deal with insurers, leaving the local brokers to advise you.

This approach can sometimes slow the quotation process and result in greater cost. It is worth asking how your broker will work for you.

It is not uncommon for law firms to have three brokers in a chain between them and their insurer (without knowing it).

It can lead to higher costs, as each broker takes a fee. It also creates a chain of communication between you and your insurer, which can lead to an extended renewal process and drawn-out negotiations.

Gary Horswell, managing director, Ntegrity

43. What is a ‘co-insurance’ facility and what are the benefits to my firm?

A 'co-insurance' facility refers to an arrangement where multiple insurers jointly underwrite a single policy, each taking a proportion of the risk and premium. For example, three insurers might each take a 33.3% share of the liability of a firm’s PII cover. The one appointed ‘lead insurer’ will deal with the conduct of any claims.

The potential benefits to a firm are as follows:

- Increased capacity – co-insurance allows firms, especially larger or higher-risk practices, to access greater levels of cover than a single insurer might be willing to provide alone.

- Risk diversification – by spreading the risk across several insurers, your firm is less exposed to the financial instability or withdrawal of any one insurer.

- Market access – co-insurance facilities are usually managed by specialist brokers with strong insurer relationships. This can improve access to competitive terms and tailored cover.

- Pricing stability – with multiple insurers involved, pricing may be more stable and less prone to sudden increases due to individual insurer strategy changes.

- Claims support – brokers managing co-insurance facilities often provide enhanced claims support and risk management services, helping firms to navigate complex claims scenarios.

However, firms should be aware that co-insurance can also mean more complex claims handling, as multiple insurers may need to agree on liability and settlement. It’s essential to work with a broker experienced in managing these arrangements.

Neil Pointon, divisional director, Howden

44. What is ‘broker duplication’?

Broker duplication is where an insurer receives a law firm’s proposal form from more than one broker.

This can reflect badly on the firm and should be avoided where possible. If you have more than one broker involved in sourcing terms, give explicit instructions as to which insurers they can and cannot approach directly on behalf of your firm.

Brian Boehmer, partner, Lockton

45. What is a Managing General Agent (MGA)?

From a law firm’s standpoint, a Managing General Agent is for all intents and purposes an insurer, but it does not take on the risk itself.

An MGA is a specialised type of insurance agent that has been granted underwriting authority by an insurer (or reinsurer) to administer programs on its behalf. The MGA writes policies and takes a share of any profits, and the insurer (or reinsurer) takes the risk and pays for any claims arising.

MGAs are specialists in their space. While insurance companies may change their strategies and switch in and out of particular insurance markets over time, MGAs offer stability to the market by their ability to change the insurance companies backing them.

Dan Blundell, senior vice president, Paragon

46. What is the Participating Insurers Agreement (PIA)?

This is the agreement that insurers sign up to in order to be allowed to insure an SRA-regulated legal practice. So it covers England and Wales.

The PIA sets out the terms and conditions to provide professional indemnity insurance, including the Minimum Terms and Conditions (see 36).

Dan Blundell, senior vice president, Paragon

47. What are reserves and how do they affect my premiums?

Reserves are funds that insurers set aside to cover future claims and liabilities. These reserves are a critical part of an insurer’s financial strategy and regulatory compliance, ensuring they can meet obligations to policyholders even in adverse conditions.

Insurers may set a reserve as soon as a claim is notified and liability and ‘quantum’ (cost) are clear, or at any point once an insurer is satisfied that liability is likely and quantum can be reasonably estimated. The reserve represents the insurer’s best estimate of the financial exposure associated with a claim, including damages and both claimant and defence costs.

Reserves are not fixed – they can increase or decrease as the claim progresses and more information becomes available. If a claim is ultimately withdrawn or successfully defended, the reserve will usually be removed entirely.

Insurers typically provide a breakdown of each claim reserve, distinguishing between the estimated damages payment and defence costs. Claimant’s costs are usually incorporated into the damages reserve, because of the way insurers treat claimant’s costs, and also because settlement payments are often made on a “costs-inclusive” basis, so it can be difficult to attribute a precise figure to them.

Large reserves can lead to higher premiums, even if no payment is ultimately made. This is because insurers use reserves to assess future risk. However, reserves are inherently uncertain and may not always reflect the true outcome of a claim, especially in complex or evolving disputes. If you believe a reserve is incorrect, discuss this with your broker/insurer.

Neil Pointon, divisional director, Howden

"Take time to focus on what you’re doing, who you’re doing it for and how much it could cost if you’re found liable for their loss. Effective and robust risk management processes could help avoid notifications being made against your firm in the first place."

James Kerr, vice president (Europe), Travelers

Why do law firms choose Travelers?

It’s because Travelers has unmatched expertise and longevity in the legal sector, with a dedicated team of experts in underwriting, claims and risk management.

See also:

- Professional indemnity insurance for law firms FAQs: Part one (How to keep your PI insurance costs down; The PI insurance application process)

- Five highly practical factsheets explaining how to avoid professional negligence claims in residential conveyancing, wills and probate, commercial property, company and commercial, and commercial litigation

- Client onboarding that reduces risk